Cleaning TRACE Corporate Bond Data: A Walkthrough#

This notebook walks through an end-to-end pipeline for cleaning FINRA TRACE corporate bond transaction data. We start from raw intraday trade reports and progress through filtering, error correction, and daily aggregation to produce an enriched panel with duration, convexity, and credit spreads.

We use a January–February 2024 sample window throughout. The same pipeline runs identically on the full 2002–present history.

import os

import sys

from pathlib import Path

# Ensure src/ is importable regardless of where the notebook executes from.

# When run via dodo.py the cwd is the project root; when run from _output/

# we walk up to find the src/ directory.

_cwd = Path.cwd()

_candidates = [_cwd / "src", _cwd.parent / "src", _cwd]

for _p in _candidates:

if (_p / "settings.py").exists():

sys.path.insert(0, str(_p))

os.chdir(_p.parent) # set project root as cwd

break

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

import numpy as np

import polars as pl

from settings import config

DATA_DIR = Path(config("DATA_DIR"))

PULL_DIR = DATA_DIR / "pulled"

plt.rcParams.update({

"figure.figsize": (10, 4),

"axes.titlesize": 13,

"axes.labelsize": 11,

"figure.dpi": 120,

})

1. What Is TRACE and Why Does Cleaning Matter?#

TRACE (Trade Reporting and Compliance Engine) is operated by FINRA. Every over-the-counter (OTC) corporate bond trade in the United States must be reported to TRACE within 15 minutes of execution. TRACE Enhanced, available from July 2002, provides the most complete data: counterparty identifiers, the full trade lifecycle (original reports, corrections, cancellations, reversals), and both price and volume.

What securities does TRACE cover?#

While this project focuses on corporate bonds, TRACE covers several categories of fixed-income securities:

Corporate bonds (investment-grade, high-yield, and convertible debt)—reported since TRACE launched in July 2002. This is the asset class we work with here.

Agency debentures—reported since March 2010.

Mortgage-backed securities (MBS) and asset-backed securities (ABS), including TBA transactions—reported since May 2011; public dissemination was phased in through 2015.

U.S. Treasury securities—reported since July 2017, but transaction-level public dissemination only began in March 2024, limited to on-the-run nominal coupons on an end-of-day basis. Full Treasury transaction data is not available to the public or researchers.

Rule 144A private placements—reported separately; included in our pipeline via the TRACE 144A feed.

What information is in the public data?#

The corporate bond transaction data that FINRA makes available to the public and to academics includes trade-level details (price, yield, volume, execution time, buy/sell indicator, counterparty type), but dealer identity is either removed or masked. The TRACE Enhanced data available on WRDS does not contain unmasked dealer identifiers.

Data access#

WRDS is the most common academic access point for corporate bond TRACE data (Enhanced, Standard, and 144A feeds). WRDS does not host agency, MBS/ABS, or Treasury TRACE data.

FINRA also makes corporate bond TRACE data available directly to academic institutions and to the public (with delays). MBS/ABS historical data requires a separate agreement with FINRA. Free next-day transaction data and aggregate reports are available on FINRA’s website for non-commercial use.

Unlike equities, which trade on centralized exchanges with a consolidated limit order book, corporate bonds trade OTC through dealer intermediaries. This creates fundamental data-quality challenges:

No consolidated best bid/offer. Prices reflect individually negotiated trades between dealers and customers or between dealers.

Market microstructure noise (MMN) is substantially larger than in equities. Transaction prices contain bid-ask bounce and dealer markups.

Trade lifecycle records. A single economic trade can generate multiple TRACE records (original report, cancellation, correction, reversal).

Using uncleaned TRACE data leads to biased return estimates and spurious factor premia—a problem documented extensively in recent research.

Why this pipeline exists: lessons from the literature#

Dickerson, Robotti, and Rossetti (2024), “Common pitfalls in the evaluation of corporate bond strategies” (SSRN 4575879):

Large abnormal returns documented for many corporate bond strategies are primarily artifacts of (a) ignoring market microstructure noise in transaction-based prices and (b) applying ex-post (asymmetric) data filtering.

MMN magnitude: The short-term reversal premium drops from 0.90% per month to approximately zero after correcting for MMN. Price-based signals (credit spread, yield) show 50–65% reductions in return premiums.

Ex-post filtering bias: Out of 480 ex-ante filtered strategies, only 2 (0.4%) produce significant momentum premia. With ex-post filtering, that number jumps to 119 (25%)—almost entirely an artifact.

Recommendation: Use an “implementation gap” (source signal prices at least one day before month-end execution prices) and apply only ex-ante filters with information available at portfolio formation.

Dickerson, Robotti, and Rossetti (2026), “The Corporate Bond Factor Replication Crisis”:

Evaluates 108 signals across 9 thematic clusters using the Open Bond Asset Pricing (OBAP) framework.

Two sources systematically inflate reported premia: (a) OTC microstructure that prevents execution at signal-formation prices, and (b) ex-post filtering that embeds future information into portfolio construction.

Result: The majority of previously documented anomalies fail—they are artifacts of measurement error, not genuine risk premia.

Provides an open-source end-to-end TRACE data pipeline (the basis for the Stage 0 cleaning code in this project).

Pipeline overview#

Raw TRACE Enhanced --[FISD filter]--> FISD-filtered --[11 filters + daily agg]--> Stage 0

(intraday trades) (standard US (daily panel)

corporate bonds) |

v

Stage 1 <--[QuantLib + ratings + linker]

(enriched panel: duration, convexity,

credit spreads, ratings, equity IDs)

2. Data Sources and Pipeline Overview#

The pipeline consumes 14 datasets from four providers: WRDS (TRACE trade feeds and FISD bond reference tables), the Liu-Wu yield curve (Google Sheets), the Kenneth French Data Library (Dartmouth), and the Open Source Bond Asset Pricing project (openbondassetpricing.com). These fall into three groups: trade data (the raw transactions we clean), bond reference data (characteristics, ratings, and identifiers we merge in), and validation / linkage data (external benchmarks and cross-asset links).

# |

Dataset |

Source |

Pipeline role |

Stage |

|---|---|---|---|---|

1 |

TRACE Enhanced |

WRDS |

Primary trade data (Jul 2002–Sep 2024) |

Pull \(\to\) FISD filter \(\to\) Stage 0 \(\to\) Stage 1 |

2 |

TRACE Standard |

WRDS |

Extends trade coverage (Oct 2024+) |

Pull \(\to\) FISD filter \(\to\) Stage 0 \(\to\) Stage 1 |

3 |

TRACE 144A |

WRDS |

Private-placement trades (Rule 144A) |

Pull \(\to\) FISD filter \(\to\) Stage 0 \(\to\) Stage 1 |

4 |

FISD Issue |

WRDS |

Bond-level reference (coupon, maturity, offering) |

Pre-processing + Stage 1 |

5 |

FISD Issuer |

WRDS |

Issuer attributes (SIC code, country) |

Pre-processing |

6 |

FISD Amount Outstanding |

WRDS |

Time-varying par amount outstanding |

Stage 1 |

7 |

FISD Ratings (S&P) |

WRDS |

Historical S&P credit ratings |

Stage 1 |

8 |

FISD Ratings (Moody’s) |

WRDS |

Historical Moody’s credit ratings |

Stage 1 |

9 |

FISD Redemption |

WRDS |

Callable-bond flag |

Stage 1 |

10 |

Liu-Wu Treasury Yields |

Google Sheets |

Zero-coupon yield curve for credit spreads |

Stage 1 |

11 |

Fama-French SIC Codes |

Dartmouth |

Industry classification (FF-17 / FF-30) |

Stage 1 |

12 |

OSBAP Linker (Fang, 2025) |

OSBAP |

Bond-to-equity identifier mapping |

Stage 1 |

13 |

OSBAP Corporate Bond Returns |

OSBAP |

Validation benchmark (duration, spreads) |

Testing only |

14 |

OSBAP Treasury Bond Returns |

OSBAP |

Not currently consumed |

— |

Three TRACE feeds#

FINRA publishes corporate bond trades through three separate reporting channels. The pipeline pulls all three and merges them after cleaning:

Enhanced is the workhorse dataset. It has the longest history (July 2002 onward), the richest columns (exact volume in

entrd_vol_qt, counterparty IDs incntra_mp_id), and is the target of most academic TRACE-cleaning papers.Standard is the real-time public feed. WRDS makes it available from October 2024, so it extends coverage into months where Enhanced is not yet released. It uses a slightly different column schema (

ascii_rptd_vol_txfor volume,sideinstead ofrpt_side_cd).144A captures a separate market segment: bonds sold to qualified institutional buyers under SEC Rule 144A. These private placements do not appear in the Enhanced or Standard feeds.

When the three are combined in Stage 1, Enhanced takes priority. Standard is clipped to dates after the Enhanced maximum date to avoid overlap, while 144A rows are kept unconditionally (they cover distinct bonds). Duplicate (cusip, date) pairs across feeds are resolved with preference Enhanced > Standard > 144A.

FISD reference data (6 files)#

The Mergent Fixed Income Securities Database (FISD), accessed via WRDS, provides the bond-level reference data that the pipeline relies on throughout:

FISD Issue — One row per bond. Coupon, maturity, offering date, offering amount, bond type, currency, and other characteristics. Combined with FISD Issuer to build the FISD universe of standard US corporate bonds (10 screens: USD only, fixed-rate, non-convertible, non-ABS, etc.). Also used in Stage 1 to map

issue_idto CUSIP for ratings and amount-outstanding merges.FISD Issuer — One row per issuer. Provides the SIC code (used for Fama-French industry classification) and country of domicile.

FISD Amount Outstanding History — Time-varying par amount. Merged into the Stage 1 panel via

merge_asof(backward on date) so each bond-day observation reflects the most recent outstanding amount.FISD Ratings (S&P) and FISD Ratings (Moody’s) — Historical credit ratings (one row per rating event). Converted to numeric scales in Stage 1 and merged via

merge_asofso each bond-day gets the most recent rating. A composite rating is computed as the average of the S&P and Moody’s numeric scores.FISD Redemption — Callable/redeemable flags. Produces a binary

callableindicator merged into Stage 1.

Liu-Wu Treasury yields#

The Liu-Wu zero-coupon Treasury yield curve (sourced from a Google Sheets mirror of the original Liu-Wu dataset) provides daily yields at 1, 2, 5, 7, 10, 20, and 30-year maturities. Stage 1 interpolates this curve at each bond’s remaining maturity and subtracts the duration-matched Treasury yield from the bond’s yield-to-maturity to compute the credit spread.

Fama-French SIC codes#

The Kenneth French Data Library provides mappings from SIC code ranges

to the Fama-French 17-industry and 30-industry classification systems.

In Stage 1, each bond issuer’s SIC code (from FISD Issuer) is matched

to these ranges, adding ff17num and ff30num industry identifiers

to every bond-day observation.

Open Source Bond Asset Pricing (OSBAP) datasets#

The OSBAP project at openbondassetpricing.com provides three files that play different roles:

OSBAP Linker (Fang, 2025) — A core Stage 1 input. Maps issuer CUSIPs (first 6 characters) to equity identifiers (PERMNO, PERMCO, GVKEY) over time. Many bonds are issued through subsidiaries that do not share the parent’s identifiers, and 19% of CUSIP-6s change ultimate parents during the sample. The linker resolves this using CUSIP-ticker mappings from ICE and TRACE, the ticker-GVKEY mapping from Compustat, and the CRSP-Compustat link, with extensive hand corrections. Forward-filled and left-joined on (issuer CUSIP, year-month) in Stage 1 Step 7.

OSBAP Corporate Bond Returns — A validation-only benchmark. The test suite (

test_stage1_vs_open_source.py) aggregates Stage 1 daily output to month-end, inner-joins with OSBAP on (cusip, date), and checks that yield-to-maturity, modified duration, convexity, credit spread, time-to-maturity, bond market cap, bond age, and industry classifications are highly correlated and within acceptable tolerance. This is how we confirm the pipeline is producing correct results.OSBAP Treasury Bond Returns — Pulled for completeness but not currently consumed by any processing or validation stage.

3. Raw TRACE Enhanced Data#

Each row in raw TRACE is a single trade report. Key columns:

Column |

Description |

|---|---|

|

9-character bond identifier |

|

Execution date and time |

|

Reported price per $100 par |

|

Par volume traded |

|

Yield at time of trade |

|

Status code: T = original trade, X = cancellation, C = correction, W/Y = reversal |

|

B = buy, S = sell (from reporting dealer perspective) |

|

Counterparty: C = customer, D = inter-dealer |

|

Sequence numbers for matching corrections to originals |

raw = pl.scan_parquet(

PULL_DIR / "trace_enhanced" / "**/*.parquet",

hive_partitioning=True,

missing_columns="insert",

).filter(pl.col("year") == 2024, pl.col("month") == 1)

n_raw = raw.select(pl.len()).collect().item()

cols_raw = raw.collect_schema().names()

print(f"Raw TRACE Enhanced (Jan 2024) -- Rows: {n_raw:,} | Columns: {len(cols_raw)}")

Raw TRACE Enhanced (Jan 2024) -- Rows: 3,768,457 | Columns: 21

Example rows#

raw.head(10).collect()

| cusip_id | bond_sym_id | trd_exctn_dt | trd_exctn_tm | days_to_sttl_ct | lckd_in_ind | wis_fl | sale_cndtn_cd | msg_seq_nb | trc_st | trd_rpt_dt | trd_rpt_tm | entrd_vol_qt | rptd_pr | yld_pt | asof_cd | orig_msg_seq_nb | rpt_side_cd | cntra_mp_id | year | month |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| str | str | date | i64 | str | str | str | str | str | str | date | i64 | f64 | f64 | f64 | str | str | str | str | i64 | i64 |

| "02209SBD4" | "MO4797929" | 2024-01-01 | null | null | null | "N" | null | "0000453" | "T" | 2024-01-02 | null | 3000.0 | 100.049 | 4.787982 | "A" | null | "B" | "D" | 2024 | 1 |

| "02209SBD4" | "MO4797929" | 2024-01-01 | null | null | null | "N" | null | "0000555" | "T" | 2024-01-02 | null | 3000.0 | 100.049 | 4.787982 | "A" | null | "S" | "D" | 2024 | 1 |

| "254687FS0" | "DIS4969022" | 2024-01-01 | null | null | null | "N" | null | "0000479" | "T" | 2024-01-02 | null | 5000.0 | 97.448 | 4.872966 | "A" | null | "B" | "D" | 2024 | 1 |

| "254687FS0" | "DIS4969022" | 2024-01-01 | null | null | null | "N" | null | "0000547" | "T" | 2024-01-02 | null | 5000.0 | 97.448 | 4.872966 | "A" | null | "S" | "D" | 2024 | 1 |

| "30303M8J4" | "FB5522214" | 2024-01-01 | null | null | null | "N" | null | "0000474" | "T" | 2024-01-02 | null | 10000.0 | 92.531 | 4.940009 | "A" | null | "B" | "D" | 2024 | 1 |

| "30303M8J4" | "FB5522214" | 2024-01-01 | null | null | null | "N" | null | "0000558" | "T" | 2024-01-02 | null | 10000.0 | 92.531 | 4.940009 | "A" | null | "S" | "D" | 2024 | 1 |

| "404280DH9" | "HBC5458071" | 2024-01-01 | null | null | null | "N" | null | "0000072" | "T" | 2024-01-02 | null | 2e6 | 101.0 | null | "A" | null | "S" | "A" | 2024 | 1 |

| "458140BX7" | "INTC5238071" | 2024-01-01 | null | null | null | "N" | null | "0000477" | "T" | 2024-01-02 | null | 10000.0 | 69.707 | 4.993 | "A" | null | "B" | "D" | 2024 | 1 |

| "458140BX7" | "INTC5238071" | 2024-01-01 | null | null | null | "N" | null | "0000566" | "T" | 2024-01-02 | null | 10000.0 | 69.707 | 4.993 | "A" | null | "S" | "D" | 2024 | 1 |

| "46647PCQ7" | "JPM5260072" | 2024-01-01 | null | null | null | "N" | null | "0000676" | "T" | 2024-01-02 | null | 3e6 | 98.89 | null | "A" | null | "B" | "A" | 2024 | 1 |

raw.tail(10).collect().glimpse()

Rows: 10

Columns: 21

$ cusip_id <str> 'Y8085FBU3', 'Y8085FBU3', 'Y8085FBU3', 'Y8846QAG1', 'Y8846QAG1', 'Y8846QAG1', 'Y8846QAG1', 'Y8850AAB0', 'Y93541AA1', 'Y93541AA1'

$ bond_sym_id <str> 'HXSCF5730863', 'HXSCF5730863', 'HXSCF5730863', 'PTFRF4937561', 'PTFRF4937561', 'PTFRF4937561', 'PTFRF4937561', 'TNABY4760205', 'CHVKF4590832', 'CHVKF4590832'

$ trd_exctn_dt <date> 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31

$ trd_exctn_tm <i64> null, null, null, null, null, null, null, null, null, null

$ days_to_sttl_ct <str> null, null, null, null, null, null, null, null, null, null

$ lckd_in_ind <str> null, null, null, null, null, null, null, null, null, null

$ wis_fl <str> 'N', 'N', 'N', 'N', 'N', 'N', 'N', 'N', 'N', 'N'

$ sale_cndtn_cd <str> null, null, null, null, null, null, null, null, null, null

$ msg_seq_nb <str> '0040572', '0040573', '0087790', '0001307', '0001333', '0002973', '0007559', '0093183', '0004037', '0004038'

$ trc_st <str> 'T', 'T', 'T', 'T', 'T', 'T', 'T', 'T', 'T', 'T'

$ trd_rpt_dt <date> 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31, 2024-01-31

$ trd_rpt_tm <i64> null, null, null, null, null, null, null, null, null, null

$ entrd_vol_qt <f64> 200000.0, 200000.0, 400000.0, 1600000.0, 1600000.0, 200000.0, 1000000.0, 210000.0, 1000000.0, 1000000.0

$ rptd_pr <f64> 101.11, 101.11, 101.153, 98.625, 98.625, 98.63, 98.55, 99.911, 63.875, 63.875

$ yld_pt <f64> null, null, null, null, null, null, null, null, null, null

$ asof_cd <str> null, null, null, null, null, null, null, null, null, null

$ orig_msg_seq_nb <str> null, null, null, null, null, null, null, null, null, null

$ rpt_side_cd <str> 'S', 'B', 'S', 'S', 'B', 'B', 'B', 'B', 'S', 'B'

$ cntra_mp_id <str> 'C', 'A', 'C', 'A', 'C', 'C', 'C', 'C', 'C', 'A'

$ year <i64> 2024, 2024, 2024, 2024, 2024, 2024, 2024, 2024, 2024, 2024

$ month <i64> 1, 1, 1, 1, 1, 1, 1, 1, 1, 1

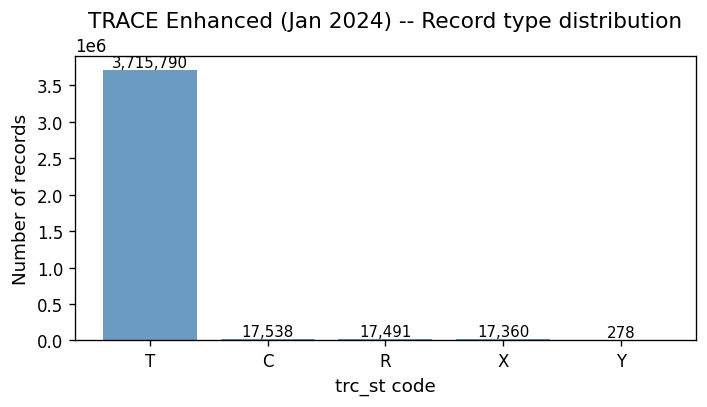

TRACE status code distribution#

The trc_st column tells us whether a record is an original trade (T),

a cancellation (X), a correction (C), or a reversal (W/Y).

Only status-T records represent actual trades. The rest are amendments to

prior records and must be matched and handled by the Dick-Nielsen cleaning

procedure.

trc_st_dist = (

raw.group_by("trc_st")

.agg(pl.len().alias("n"))

.sort("n", descending=True)

.collect()

)

fig, ax = plt.subplots(figsize=(6, 3.5))

bars = ax.bar(

trc_st_dist["trc_st"].to_list(),

trc_st_dist["n"].to_list(),

color="steelblue",

alpha=0.8,

)

for bar, val in zip(bars, trc_st_dist["n"].to_list()):

ax.text(

bar.get_x() + bar.get_width() / 2,

bar.get_height(),

f"{val:,}",

ha="center",

va="bottom",

fontsize=9,

)

ax.set_ylabel("Number of records")

ax.set_xlabel("trc_st code")

ax.set_title("TRACE Enhanced (Jan 2024) -- Record type distribution")

fig.tight_layout()

plt.show()

The large number of C (correction) and X (cancellation) records is exactly why the Dick-Nielsen cleaning procedure exists. These are not separate trades—they are amendments to prior trade reports.

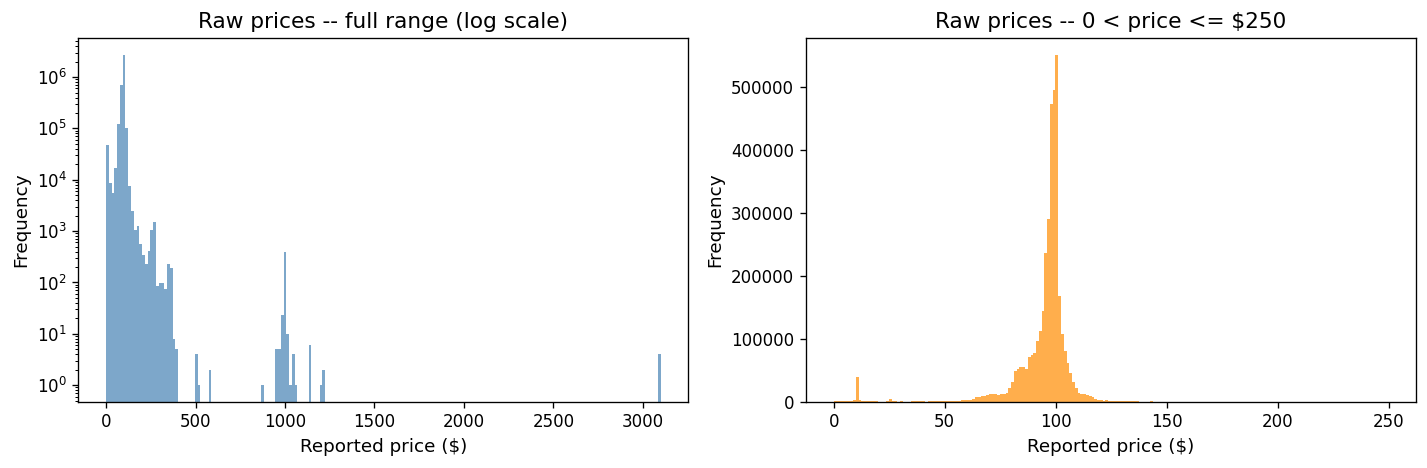

Raw price distribution#

Raw data contains extreme prices from decimal-shift errors, data entry mistakes, and pre-cancellation records. The log-scale histogram reveals a long tail, while the right panel shows the “true” distribution concentrated near par (~100).

raw_prices = raw.select("rptd_pr").collect()["rptd_pr"].to_numpy()

fig, axes = plt.subplots(1, 2, figsize=(12, 4))

axes[0].hist(

raw_prices[np.isfinite(raw_prices)],

bins=200,

color="steelblue",

alpha=0.7,

edgecolor="none",

)

axes[0].set_xlabel("Reported price ($)")

axes[0].set_ylabel("Frequency")

axes[0].set_title("Raw prices -- full range (log scale)")

axes[0].set_yscale("log")

mask = (raw_prices > 0) & (raw_prices <= 250)

axes[1].hist(raw_prices[mask], bins=200, color="darkorange", alpha=0.7, edgecolor="none")

axes[1].set_xlabel("Reported price ($)")

axes[1].set_ylabel("Frequency")

axes[1].set_title("Raw prices -- 0 < price <= $250")

fig.tight_layout()

plt.show()

print(f"Prices <= 0: {(raw_prices <= 0).sum():,}")

print(f"Prices > 1000: {(raw_prices[np.isfinite(raw_prices)] > 1000).sum():,}")

print(f"Null prices: {np.isnan(raw_prices).sum():,}")

Prices <= 0: 0

Prices > 1000: 29

Null prices: 0

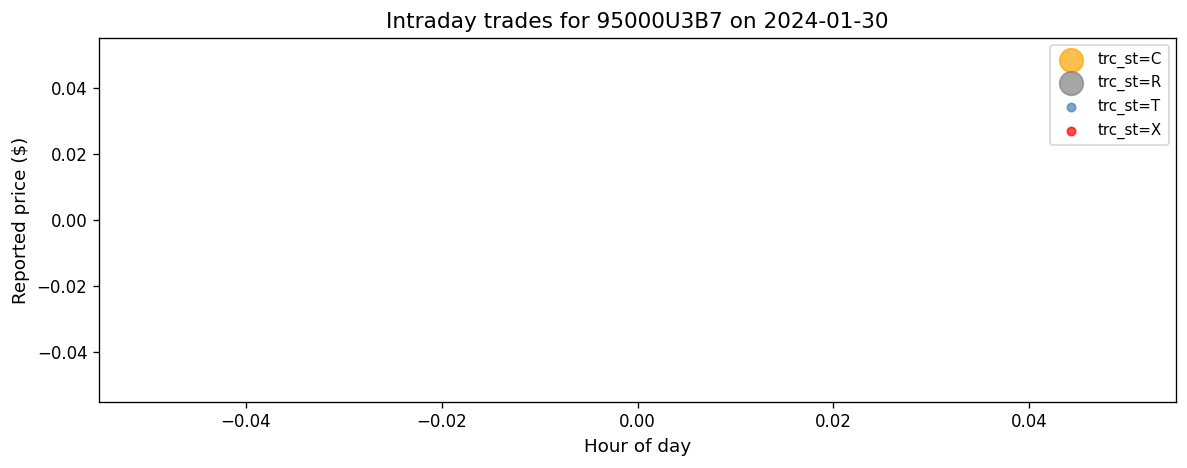

A single bond’s intraday trades#

To build intuition, let’s look at a single well-traded bond across one day. We plot every TRACE record colored by its status code.

top_cusips = (

raw.filter(pl.col("trc_st") == "T")

.group_by("cusip_id")

.agg(pl.len().alias("n"))

.sort("n", descending=True)

.head(5)

.collect()

)

print("Top 5 CUSIPs by original-trade count (Jan 2024):")

top_cusips

Top 5 CUSIPs by original-trade count (Jan 2024):

| cusip_id | n |

|---|---|

| str | u32 |

| "95000U3B7" | 16722 |

| "126650CX6" | 5750 |

| "06051GFM6" | 5477 |

| "718172CW7" | 4992 |

| "20030NCT6" | 4384 |

# Find a cusip-date pair that has multiple status codes (T, C, X, etc.)

# so the scatter plot illustrates the lifecycle records.

_cusip_date_mix = (

raw.group_by("cusip_id", "trd_exctn_dt")

.agg(

pl.col("trc_st").n_unique().alias("n_status"),

pl.len().alias("n_records"),

)

.filter(pl.col("n_status") >= 3)

.sort("n_records", descending=True)

.head(1)

.collect()

)

# Fall back to the most-traded cusip on 2024-01-16 if no multi-status pair found

if len(_cusip_date_mix) > 0:

example_cusip = _cusip_date_mix["cusip_id"][0]

example_date = _cusip_date_mix["trd_exctn_dt"][0]

else:

example_cusip = top_cusips["cusip_id"][0]

example_date = None

intraday = (

raw.filter(

(pl.col("cusip_id") == example_cusip)

& (

(pl.col("trd_exctn_dt") == example_date)

if example_date is not None

else (pl.col("trd_exctn_dt") == pl.lit("2024-01-16").str.to_date())

)

)

.sort("trd_exctn_tm")

.collect()

)

# If the chosen date is empty, fall back to the first available date

if len(intraday) == 0:

first_date = (

raw.filter(pl.col("cusip_id") == example_cusip)

.select(pl.col("trd_exctn_dt").min())

.collect()

.item()

)

intraday = (

raw.filter(

(pl.col("cusip_id") == example_cusip)

& (pl.col("trd_exctn_dt") == first_date)

)

.sort("trd_exctn_tm")

.collect()

)

# Convert trd_exctn_tm to hours for plotting

tm_col = intraday["trd_exctn_tm"]

if tm_col.dtype in (pl.Int64, pl.UInt64, pl.Float64):

times_hrs = tm_col.to_numpy().astype("float64") / 1e9 / 3600

elif tm_col.dtype == pl.Duration:

times_hrs = tm_col.dt.total_seconds().to_numpy().astype("float64") / 3600

elif tm_col.dtype == pl.Time:

times_hrs = (

tm_col.dt.hour().cast(pl.Float64)

+ tm_col.dt.minute().cast(pl.Float64) / 60

+ tm_col.dt.second().cast(pl.Float64) / 3600

).to_numpy()

else:

# String HH:MM:SS

parts = tm_col.str.split(":")

times_hrs = (

parts.list.get(0).cast(pl.Float64)

+ parts.list.get(1).cast(pl.Float64) / 60

+ parts.list.get(2).cast(pl.Float64) / 3600

).to_numpy()

trade_date = intraday["trd_exctn_dt"][0]

prices = intraday["rptd_pr"].to_numpy()

statuses = intraday["trc_st"].to_list()

colors_map = {"T": "steelblue", "X": "red", "C": "orange", "W": "purple", "Y": "green"}

fig, ax = plt.subplots(figsize=(10, 4))

for status in sorted(set(statuses)):

mask_s = np.array([s == status for s in statuses])

size = 200 if status in ("C", "R") else 25

ax.scatter(

times_hrs[mask_s],

prices[mask_s],

label=f"trc_st={status}",

alpha=0.7,

s=size,

color=colors_map.get(status, "gray"),

)

ax.set_xlabel("Hour of day")

ax.set_ylabel("Reported price ($)")

ax.set_title(f"Intraday trades for {example_cusip} on {trade_date}")

ax.legend(fontsize=9)

fig.tight_layout()

plt.show()

print(f"Total records: {len(intraday)}")

for st in sorted(set(statuses)):

print(f" trc_st={st}: {statuses.count(st)}")

Total records: 10192

trc_st=C: 1

trc_st=R: 1

trc_st=T: 5126

trc_st=X: 5064

Cancellations (red) and corrections (orange) are not independent trades.

They reference prior records via orig_msg_seq_nb and must be matched and

removed or replaced. This is the job of the Dick-Nielsen procedure.

4. FISD Universe Filtering#

Before cleaning trade data, we restrict to standard US corporate bonds using the Mergent Fixed Income Securities Database (FISD). The universe is built with these screens:

USD denominated only

Fixed-rate coupon (exclude variable)

Non-convertible

Non-asset-backed

Exclude government, municipal, MBS, ABS, and other non-corporate types

Valid coupon frequency

Complete accrual fields (offering_date, dated_date)

Principal amount = $1,000

Exclude equity-linked / index-linked bonds

Tenor >= 1 year

We then inner-join TRACE on cusip_id with the FISD universe, dropping all

non-matching bonds.

fisd = pl.scan_parquet(DATA_DIR / "fisd_universe.parquet")

n_fisd = fisd.select(pl.len()).collect().item()

print(f"FISD Universe: {n_fisd:,} bonds")

FISD Universe: 111,727 bonds

Example bonds from the FISD universe#

fisd.head(5).collect()

| complete_cusip | issue_id | issue_name | issuer_id | foreign_currency | coupon_type | coupon | convertible | asset_backed | rule_144a | bond_type | private_placement | interest_frequency | dated_date | day_count_basis | offering_date | maturity | principal_amt | offering_amt | country_domicile | sic_code | tenor |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| str | f64 | str | f64 | str | str | f64 | str | str | str | str | str | i64 | date | str | date | date | f64 | f64 | str | str | f64 |

| "000361AA3" | 1.0 | "NT" | 3.0 | "N" | "F" | 9.5 | "N" | "N" | "N" | "CDEB" | "N" | 2 | 1989-11-01 | "30/360" | 1989-10-24 | 2001-11-01 | 1000.0 | 65000.0 | "USA" | "3720" | 12.021903 |

| "000361AB1" | 2.0 | "NT" | 3.0 | "N" | "F" | 7.25 | "N" | "N" | "N" | "CDEB" | "N" | 2 | 1993-10-15 | "30/360" | 1993-10-12 | 2003-10-15 | 1000.0 | 50000.0 | "USA" | "3720" | 10.006845 |

| "00077DAB5" | 3.0 | "MTN" | 40263.0 | "N" | "F" | 4.15 | "N" | "N" | "N" | "CMTN" | "N" | 2 | 1994-01-14 | "30/360" | 1994-01-07 | 1996-01-12 | 1000.0 | 100000.0 | "USA" | "6029" | 2.01232 |

| "00077DAF6" | 4.0 | "SUB DEP NT SER B" | 40263.0 | "N" | "F" | 8.25 | "N" | "N" | "N" | "USBN" | "N" | 2 | 1994-08-02 | "30/360" | 1994-07-27 | 2009-08-01 | 1000.0 | 200000.0 | "USA" | "6029" | 15.014374 |

| "00077TAA2" | 5.0 | "SUB DEP NT SER B" | 40263.0 | "N" | "F" | 7.75 | "N" | "N" | "N" | "CDEB" | "N" | 2 | 1993-05-15 | "30/360" | 1993-05-20 | 2023-05-15 | 1000.0 | 250000.0 | "USA" | "6029" | 29.984942 |

Raw vs FISD-filtered comparison#

fisd_filtered = pl.scan_parquet(

DATA_DIR / "trace_enhanced_fisd" / "**/*.parquet",

hive_partitioning=True,

).filter(pl.col("year") == 2024, pl.col("month") == 1)

n_fisd_filtered = fisd_filtered.select(pl.len()).collect().item()

n_cusips_raw = raw.select(pl.col("cusip_id").n_unique()).collect().item()

n_cusips_fisd = fisd_filtered.select(pl.col("cusip_id").n_unique()).collect().item()

print(f"{'':30s} {'Rows':>12s} {'Unique CUSIPs':>15s}")

print(f"{'Raw TRACE Enhanced (Jan 24)':30s} {n_raw:>12,} {n_cusips_raw:>15,}")

print(f"{'After FISD filter':30s} {n_fisd_filtered:>12,} {n_cusips_fisd:>15,}")

print(f"{'Dropped':30s} {n_raw - n_fisd_filtered:>12,} {n_cusips_raw - n_cusips_fisd:>15,}")

pct = 100 * (n_raw - n_fisd_filtered) / n_raw

print(f"\nFISD filter removes {pct:.1f}% of raw trade records.")

Rows Unique CUSIPs

Raw TRACE Enhanced (Jan 24) 3,768,457 29,998

After FISD filter 2,792,786 11,940

Dropped 975,671 18,058

FISD filter removes 25.9% of raw trade records.

The FISD filter removes trades in non-standard bonds (government, MBS, ABS, municipals, convertibles, etc.) that are not the focus of corporate bond research.

5. Stage 0: Dick-Nielsen Cleaning Pipeline#

Stage 0 applies 11 sequential filters to the FISD-filtered intraday data

and ends with daily aggregation. The implementation lives in

src/stage0/clean_trace_local.py (function _apply_filter_chain).

# |

Filter |

Purpose |

|---|---|---|

1 |

Dick-Nielsen |

Match and remove cancellations, corrections, reversals; remove agency inter-dealer duplicates |

2 |

Decimal-shift corrector |

Fix prices that are 10x, 100x, 0.1x, or 0.01x off from neighboring trades |

3 |

Trading time |

Restrict to market hours (disabled by default) |

4 |

Trading calendar |

Remove trades on non-trading days (weekends, holidays per NYSE calendar) |

5 |

Price filter |

Remove trades with price <= 0 or > $1,000 |

6 |

Volume filter |

Remove trades with dollar volume < $10,000 |

7 |

Bounce-back filter |

Detect erroneous price spikes that revert within a few trades |

8 |

Yield-price consistency |

Remove rows where the yield field equals the price field (data entry error) |

9 |

Amount outstanding |

Remove trades with volume > 50% of offering amount |

10 |

Execution vs maturity |

Remove trades executed after the bond’s maturity date |

11 |

Initial price error |

Flag extreme price jumps in the first few trades per CUSIP |

After all filters, intraday trades are aggregated to one row per

(cusip_id, date) with equal-weighted price (prc_ew), volume-weighted

price (prc_vw), first/last prices, trade count, and total volume.

Stage 0 output: the daily panel#

s0 = pl.scan_parquet(

DATA_DIR / "stage0" / "enhanced" / "year=*/month=*/data.parquet",

hive_partitioning=True,

)

s0_jan = s0.filter(pl.col("year") == 2024, pl.col("month") == 1)

n_s0 = s0_jan.select(pl.len()).collect().item()

s0_cols = s0.collect_schema().names()

print(f"Stage 0 Enhanced (Jan 2024) -- Rows: {n_s0:,} (one row per cusip-day)")

print(f"Columns ({len(s0_cols)}): {s0_cols}")

Stage 0 Enhanced (Jan 2024) -- Rows: 149,135 (one row per cusip-day)

Columns (23): ['cusip_id', 'trd_exctn_dt', 'prc_ew', 'prc_vw', 'prc_vw_par', 'prc_first', 'prc_last', 'prc_hi', 'prc_lo', 'trade_count', 'time_ew', 'time_last', 'qvolume', 'dvolume', 'prc_bid', 'bid_last', 'bid_time_ew', 'bid_time_last', 'prc_ask', 'bid_count', 'ask_count', 'year', 'month']

Example rows#

s0_jan.head(10).collect()

| cusip_id | trd_exctn_dt | prc_ew | prc_vw | prc_vw_par | prc_first | prc_last | prc_hi | prc_lo | trade_count | time_ew | time_last | qvolume | dvolume | prc_bid | bid_last | bid_time_ew | bid_time_last | prc_ask | bid_count | ask_count | year | month |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| str | datetime[ms] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | i64 | f64 | i32 | f64 | f64 | f64 | f64 | f64 | i32 | f64 | f64 | f64 | i64 | i64 |

| "00037BAC6" | 2024-01-16 00:00:00 | 89.9055 | 89.90575 | 89.90575 | 89.905 | 89.906 | 89.906 | 89.905 | 4 | null | null | 0.16 | 0.1438492 | null | null | null | null | 89.90575 | null | 2.0 | 2024 | 1 |

| "00037BAC6" | 2024-01-24 00:00:00 | 89.658 | 89.658 | 89.658 | 89.658 | 89.658 | 89.658 | 89.658 | 1 | null | null | 1.0 | 0.89658 | null | null | null | null | 89.658 | null | 1.0 | 2024 | 1 |

| "00037BAC6" | 2024-01-30 00:00:00 | 90.477 | 90.477 | 90.477 | 90.477 | 90.477 | 90.477 | 90.477 | 1 | null | null | 0.669 | 0.605291 | 90.477 | 90.477 | null | null | null | 1.0 | 0.0 | 2024 | 1 |

| "00037BAC6" | 2024-01-31 00:00:00 | 91.183667 | 91.084617 | 91.084437 | 91.276 | 90.999 | 91.276 | 90.999 | 3 | null | null | 4.338 | 3.951243 | null | null | null | null | 90.999 | null | 1.0 | 2024 | 1 |

| "00037BAF9" | 2024-01-02 00:00:00 | 98.217 | 98.217 | 98.217 | 98.217 | 98.217 | 98.217 | 98.217 | 1 | null | null | 0.26 | 0.2553642 | null | null | null | null | 98.217 | null | 1.0 | 2024 | 1 |

| "00037BAF9" | 2024-01-03 00:00:00 | 98.611 | 98.611 | 98.611 | 98.611 | 98.611 | 98.611 | 98.611 | 2 | null | null | 2.0 | 1.97222 | null | null | null | null | 98.611 | null | 1.0 | 2024 | 1 |

| "00037BAF9" | 2024-01-24 00:00:00 | 97.731 | 97.731 | 97.731 | 97.731 | 97.731 | 97.731 | 97.731 | 1 | null | null | 0.075 | 0.073298 | null | null | null | null | 97.731 | null | 1.0 | 2024 | 1 |

| "00037BAF9" | 2024-01-29 00:00:00 | 98.303 | 98.303 | 98.303 | 98.303 | 98.303 | 98.303 | 98.303 | 1 | null | null | 0.1 | 0.098303 | 98.303 | 98.303 | null | null | null | 1.0 | 0.0 | 2024 | 1 |

| "00037BAF9" | 2024-01-30 00:00:00 | 98.14664 | 98.146641 | 98.14664 | 98.13883 | 98.15445 | 98.15445 | 98.13883 | 2 | null | null | 0.18 | 0.176664 | null | null | null | null | null | null | null | 2024 | 1 |

| "00037BAF9" | 2024-01-31 00:00:00 | 98.489 | 98.394401 | 98.394373 | 98.597 | 98.381 | 98.597 | 98.381 | 2 | null | null | 0.533 | 0.524442 | 98.394401 | 98.381 | null | null | null | 2.0 | 0.0 | 2024 | 1 |

Data reduction through the pipeline#

The table below shows how row counts change at each stage.

raw_both = pl.scan_parquet(

PULL_DIR / "trace_enhanced" / "**/*.parquet",

hive_partitioning=True,

missing_columns="insert",

).select(pl.len()).collect().item()

fisd_both = pl.scan_parquet(

DATA_DIR / "trace_enhanced_fisd" / "**/*.parquet",

hive_partitioning=True,

).select(pl.len()).collect().item()

s0_both = s0.select(pl.len()).collect().item()

summary = pl.DataFrame({

"Stage": [

"Raw TRACE Enhanced",

"After FISD filter",

"Stage 0 (daily panel)",

],

"Rows": [raw_both, fisd_both, s0_both],

"Granularity": [

"intraday trade reports",

"intraday trade reports",

"one row per cusip-day",

],

})

summary

| Stage | Rows | Granularity |

|---|---|---|

| str | i64 | str |

| "Raw TRACE Enhanced" | 423792457 | "intraday trade reports" |

| "After FISD filter" | 329061163 | "intraday trade reports" |

| "Stage 0 (daily panel)" | 26282960 | "one row per cusip-day" |

The dramatic reduction from millions of intraday records to the daily panel reflects both (a) removal of erroneous/duplicate records and (b) daily aggregation.

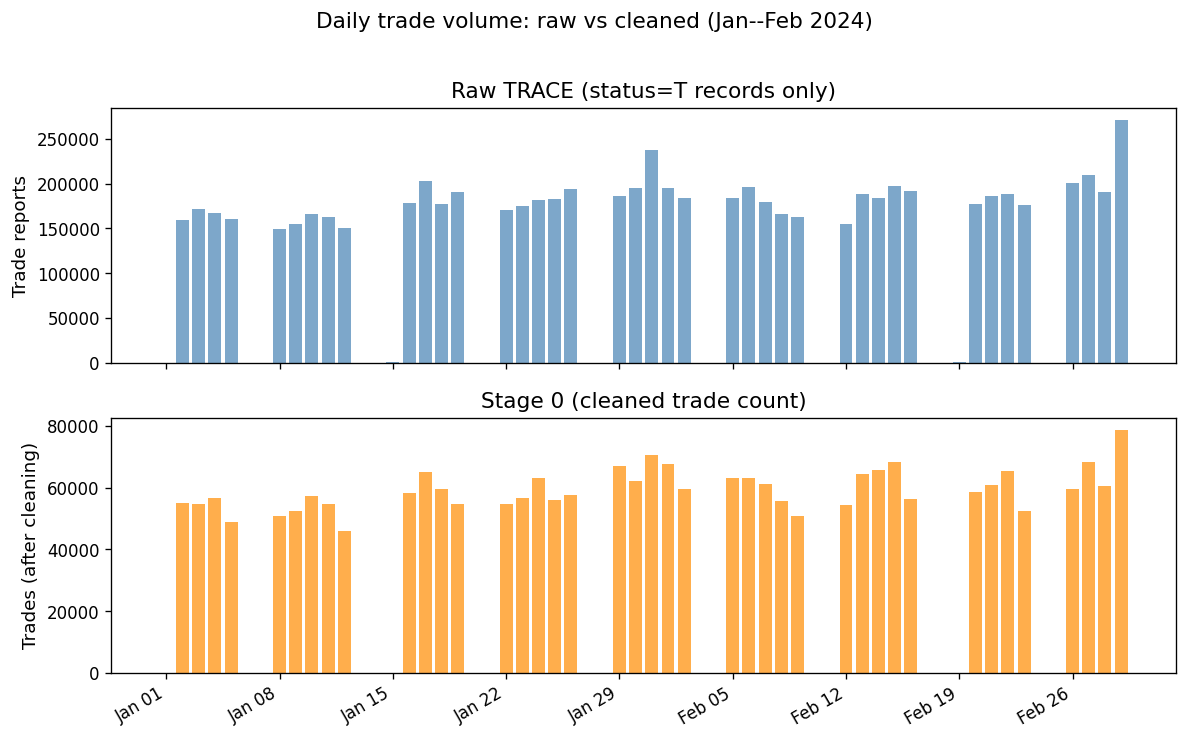

Daily trade counts: raw vs cleaned#

raw_daily = (

pl.scan_parquet(

PULL_DIR / "trace_enhanced" / "**/*.parquet",

hive_partitioning=True,

missing_columns="insert",

)

.filter(

pl.col("trc_st") == "T",

pl.col("year") == 2024,

pl.col("month").is_in([1, 2]),

)

.group_by("trd_exctn_dt")

.agg(pl.len().alias("n_trades"))

.sort("trd_exctn_dt")

.collect()

)

s0_daily = (

s0.filter(pl.col("year") == 2024, pl.col("month").is_in([1, 2]))

.group_by("trd_exctn_dt")

.agg(pl.col("trade_count").sum().alias("n_trades"))

.sort("trd_exctn_dt")

.collect()

)

fig, axes = plt.subplots(2, 1, figsize=(10, 6), sharex=True)

raw_dates = raw_daily["trd_exctn_dt"].to_pandas()

s0_dates = s0_daily["trd_exctn_dt"].to_pandas()

axes[0].bar(

raw_dates,

raw_daily["n_trades"].to_list(),

color="steelblue",

alpha=0.7,

width=0.8,

)

axes[0].set_ylabel("Trade reports")

axes[0].set_title("Raw TRACE (status=T records only)")

axes[1].bar(

s0_dates,

s0_daily["n_trades"].to_list(),

color="darkorange",

alpha=0.7,

width=0.8,

)

axes[1].set_ylabel("Trades (after cleaning)")

axes[1].set_title("Stage 0 (cleaned trade count)")

for _ax in axes:

_ax.xaxis.set_major_locator(mdates.WeekdayLocator(byweekday=mdates.MO))

_ax.xaxis.set_major_formatter(mdates.DateFormatter("%b %d"))

plt.setp(axes[1].get_xticklabels(), rotation=30, ha="right")

fig.suptitle(

"Daily trade volume: raw vs cleaned (Jan--Feb 2024)", fontsize=13, y=1.02

)

fig.tight_layout()

plt.show()

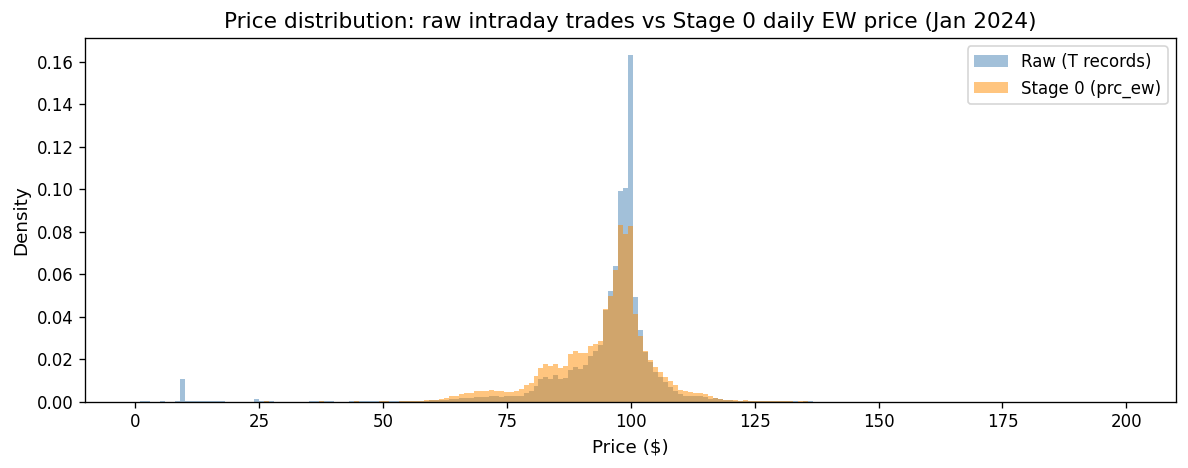

Price distributions: raw vs cleaned#

raw_pr = (

pl.scan_parquet(

PULL_DIR / "trace_enhanced" / "**/*.parquet",

hive_partitioning=True,

missing_columns="insert",

)

.filter(

(pl.col("trc_st") == "T")

& (pl.col("year") == 2024)

& (pl.col("month") == 1)

)

.select("rptd_pr")

.collect()["rptd_pr"]

.to_numpy()

)

s0_pr = (

s0_jan.select("prc_ew").collect()["prc_ew"].to_numpy()

)

fig, ax = plt.subplots(figsize=(10, 4))

bins = np.linspace(0, 200, 200)

ax.hist(

raw_pr[(raw_pr > 0) & (raw_pr <= 200)],

bins=bins,

alpha=0.5,

label="Raw (T records)",

color="steelblue",

density=True,

)

ax.hist(

s0_pr[(s0_pr > 0) & (s0_pr <= 200)],

bins=bins,

alpha=0.5,

label="Stage 0 (prc_ew)",

color="darkorange",

density=True,

)

ax.set_xlabel("Price ($)")

ax.set_ylabel("Density")

ax.set_title("Price distribution: raw intraday trades vs Stage 0 daily EW price (Jan 2024)")

ax.legend()

fig.tight_layout()

plt.show()

The cleaned distribution is tighter, with extreme tails removed. Daily aggregation (averaging across trades) further reduces noise.

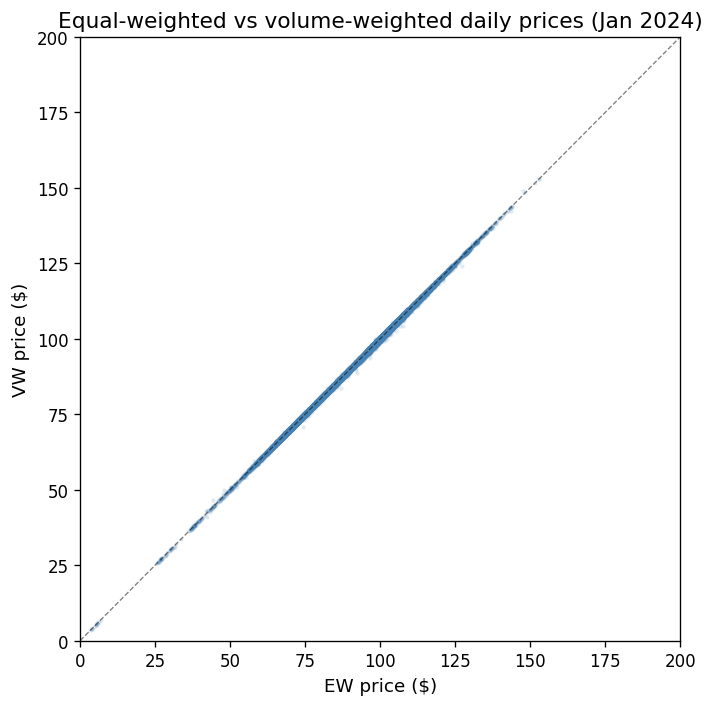

Equal-weighted vs volume-weighted prices#

The Stage 0 panel provides both prc_ew (equal-weighted average across

all intraday trades) and prc_vw (volume-weighted). For research,

volume-weighted prices down-weight small “noise” trades, providing

a better estimate of the bond’s true price.

s0_prices = (

s0_jan.select("prc_ew", "prc_vw").collect()

)

fig, ax = plt.subplots(figsize=(6, 6))

ax.scatter(

s0_prices["prc_ew"].to_numpy(),

s0_prices["prc_vw"].to_numpy(),

alpha=0.1,

s=3,

color="steelblue",

)

lims = [0, 200]

ax.plot(lims, lims, "k--", linewidth=0.8, alpha=0.5)

ax.set_xlabel("EW price ($)")

ax.set_ylabel("VW price ($)")

ax.set_title("Equal-weighted vs volume-weighted daily prices (Jan 2024)")

ax.set_xlim(lims)

ax.set_ylim(lims)

fig.tight_layout()

plt.show()

diff = np.abs(s0_prices["prc_ew"].to_numpy() - s0_prices["prc_vw"].to_numpy())

print(f"Mean |EW - VW| difference: ${np.nanmean(diff):.4f}")

print(f"Median |EW - VW| difference: ${np.nanmedian(diff):.4f}")

print(f"95th pctile |EW - VW|: ${np.nanpercentile(diff, 95):.4f}")

Mean |EW - VW| difference: $0.0629

Median |EW - VW| difference: $0.0220

95th pctile |EW - VW|: $0.2612

Market microstructure noise in context#

Most points lie on the 45-degree line, but the divergences—where small trades transact at systematically different prices than large trades—are precisely the market microstructure noise (MMN) that Dickerson, Robotti, and Rossetti (2024) warn about.

Key implications from DRR (2024):

Even after cleaning, daily prices contain MMN because individual trades include bid-ask bounce and dealer markups.

The EW price gives equal weight to a \(10K retail trade and a \)5M institutional block—yet these trades occur at systematically different prices.

The VW price partially mitigates this, but does not fully remove MMN.

Using noisy prices as signals for portfolio sorts creates spurious predictability. For example, short-term reversal premia of 0.90%/month vanish after MMN correction.

Volume-weighted prices (

prc_vw) should be preferred overprc_ewwhen computing returns for research.

6. Stage 1: Enrichment#

Stage 1 takes the clean daily panel from Stage 0 and enriches it with bond analytics and reference data:

Analytics (computed via QuantLib):

Accrued interest (to convert between clean and dirty prices)

Yield to maturity (YTM)

Modified duration and Macaulay duration

Convexity

Credit spread (bond yield minus duration-matched Liu-Wu Treasury zero-coupon yield)

Merged reference data:

FISD bond characteristics (coupon, maturity, offering amount, callable flag)

Credit ratings from Moody’s and S&P (as-of, forward-filled)

Fama-French 17/30 industry classification (via SIC codes)

Equity identifiers (PERMNO, PERMCO, GVKEY) via the OBAP bond-firm linker

import glob

s1_files = sorted(glob.glob(str(DATA_DIR / "stage1" / "stage1_*.parquet")))

s1_path = s1_files[-1] # most recent

s1 = pl.scan_parquet(s1_path)

n_s1 = s1.select(pl.len()).collect().item()

cols_s1 = s1.collect_schema().names()

print(f"Stage 1 ({Path(s1_path).name}) -- Rows: {n_s1:,} | Columns: {len(cols_s1)}")

print(f"Columns: {cols_s1}")

Stage 1 (stage1_latest.parquet) -- Rows: 27,164,296 | Columns: 43

Columns: ['cusip_id', 'permno', 'permco', 'gvkey', 'trd_exctn_dt', 'pr', 'prfull', 'acclast', 'accpmt', 'accall', 'ytm', 'mod_dur', 'mac_dur', 'convexity', 'bond_maturity', 'credit_spread', 'prc_ew', 'prc_vw_par', 'prc_first', 'prc_last', 'prc_hi', 'prc_lo', 'trade_count', 'time_ew', 'time_last', 'qvolume', 'dvolume', 'prc_bid', 'bid_last', 'bid_time_ew', 'bid_time_last', 'prc_ask', 'bid_count', 'ask_count', 'db_type', 'ff17num', 'ff30num', 'bond_age', 'bond_amt_outstanding', 'sp_rating', 'mdy_rating', 'spc_rating', 'mdc_rating']

Example rows#

s1.head(10).collect()

| cusip_id | permno | permco | gvkey | trd_exctn_dt | pr | prfull | acclast | accpmt | accall | ytm | mod_dur | mac_dur | convexity | bond_maturity | credit_spread | prc_ew | prc_vw_par | prc_first | prc_last | prc_hi | prc_lo | trade_count | time_ew | time_last | qvolume | dvolume | prc_bid | bid_last | bid_time_ew | bid_time_last | prc_ask | bid_count | ask_count | db_type | ff17num | ff30num | bond_age | bond_amt_outstanding | sp_rating | mdy_rating | spc_rating | mdc_rating |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| cat | i32 | i32 | i32 | datetime[ns] | f32 | f32 | f32 | f32 | f32 | f64 | f32 | f32 | f32 | f32 | f64 | f32 | f32 | f32 | f32 | f32 | f32 | i16 | f32 | f32 | f32 | f32 | f32 | f32 | f32 | f32 | f32 | i16 | i16 | i8 | i8 | i8 | f32 | i64 | i8 | i8 | i8 | i8 |

| "000336AE7" | 75188 | 21651 | 13557 | 2002-07-09 00:00:00 | 100.792 | 101.517693 | 0.725694 | 27.538195 | 28.263889 | 0.067082 | 4.754 | 4.913 | 27.618999 | 5.897 | 0.024732 | 100.792 | 100.792 | 100.792 | 100.792 | 100.792 | 100.792 | 1 | null | null | 0.01 | 0.010079 | null | null | null | null | 100.792 | null | 1 | 1 | 16 | 29 | 4.117728 | 100000 | 8 | 9 | 8 | 9 |

| "000336AE7" | 75188 | 21651 | 13557 | 2002-07-24 00:00:00 | 97.821999 | 98.834152 | 1.012153 | 27.538195 | 28.550346 | 0.073369 | 4.682 | 4.854 | 26.926001 | 5.856 | 0.034645 | 97.821999 | 97.821999 | 97.821999 | 97.821999 | 97.821999 | 97.821999 | 1 | null | null | 0.02 | 0.019564 | 97.821999 | 97.821999 | null | null | null | 1 | 0 | 1 | 16 | 29 | 4.158795 | 100000 | 8 | 9 | 8 | 9 |

| "000336AE7" | 75188 | 21651 | 13557 | 2002-07-25 00:00:00 | 99.099998 | 100.169441 | 1.069444 | 27.538195 | 28.607639 | 0.070631 | 4.688 | 4.853 | 26.974001 | 5.854 | 0.032801 | 99.099998 | 99.099998 | 99.099998 | 99.099998 | 99.099998 | 99.099998 | 1 | null | null | 0.025 | 0.024775 | 99.099998 | 99.099998 | null | null | null | 1 | 0 | 1 | 16 | 29 | 4.161533 | 100000 | 8 | 9 | 8 | 9 |

| "000336AE7" | 75188 | 21651 | 13557 | 2002-08-21 00:00:00 | 99.800003 | 101.327782 | 1.527778 | 27.538195 | 29.065971 | 0.069146 | 4.631 | 4.791 | 26.410999 | 5.78 | 0.033263 | 99.800003 | 99.800003 | 99.800003 | 99.800003 | 99.800003 | 99.800003 | 4 | null | null | 0.086 | 0.085828 | 99.800003 | 99.800003 | null | null | null | 4 | 0 | 1 | 16 | 29 | 4.235455 | 100000 | 8 | 9 | 8 | 9 |

| "000336AE7" | 75188 | 21651 | 13557 | 2002-08-23 00:00:00 | 99.5 | 101.104172 | 1.604167 | 27.538195 | 29.142361 | 0.069788 | 4.617 | 4.778 | 26.277 | 5.774 | 0.033632 | 99.5 | 99.5 | 99.5 | 99.5 | 99.5 | 99.5 | 1 | null | null | 0.013 | 0.012935 | 99.5 | 99.5 | null | null | null | 1 | 0 | 1 | 16 | 29 | 4.240931 | 100000 | 8 | 9 | 8 | 9 |

| "000336AE7" | 75188 | 21651 | 13557 | 2002-08-28 00:00:00 | 102.092003 | 103.753456 | 1.661458 | 27.538195 | 29.199654 | 0.064316 | 4.636 | 4.785 | 26.445999 | 5.76 | 0.028395 | 102.092003 | 102.092003 | 102.092003 | 102.092003 | 102.092003 | 102.092003 | 1 | null | null | 0.01 | 0.010209 | null | null | null | null | 102.092003 | null | 1 | 1 | 16 | 29 | 4.25462 | 100000 | 8 | 9 | 8 | 9 |

| "000336AE7" | 75188 | 21651 | 13557 | 2002-09-03 00:00:00 | 98.364998 | 100.121941 | 1.756944 | 27.538195 | 29.295139 | 0.072247 | 4.583 | 4.749 | 25.959 | 5.744 | 0.03916 | 98.364998 | 98.364998 | 98.364998 | 98.364998 | 98.364998 | 98.364998 | 1 | null | null | 0.15 | 0.147547 | null | null | null | null | 98.364998 | null | 1 | 1 | 16 | 29 | 4.271047 | 100000 | 8 | 9 | 8 | 9 |

| "000336AE7" | 75188 | 21651 | 13557 | 2002-09-20 00:00:00 | 87.551003 | 89.670792 | 2.119792 | 27.538195 | 29.657986 | 0.097752 | 4.406 | 4.622 | 24.358999 | 5.697 | 0.066524 | 87.551003 | 87.551003 | 87.530998 | 87.570999 | 87.570999 | 87.530998 | 2 | null | null | 0.2 | 0.175102 | 87.530998 | 87.530998 | null | null | 87.570999 | 1 | 1 | 1 | 16 | 29 | 4.317591 | 100000 | 8 | 9 | 8 | 9 |

| "000336AE7" | 75188 | 21651 | 13557 | 2002-09-30 00:00:00 | 91.405602 | 93.678207 | 2.272569 | 27.538195 | 29.810764 | 0.088316 | 4.432 | 4.627 | 24.568001 | 5.67 | 0.059416 | 91.405602 | 91.405602 | 91.356003 | 91.356003 | 91.480003 | 91.356003 | 5 | null | null | 0.25 | 0.228514 | 91.387032 | 91.356003 | null | null | 91.480003 | 4 | 1 | 1 | 16 | 29 | 4.344969 | 100000 | 8 | 9 | 8 | 9 |

| "000336AE7" | 75188 | 21651 | 13557 | 2002-10-23 00:00:00 | 90.144997 | 92.856804 | 2.711806 | 27.538195 | 30.25 | 0.0916 | 4.354 | 4.554 | 23.862 | 5.607 | 0.056607 | 90.144997 | 90.144997 | 90.144997 | 90.144997 | 90.144997 | 90.144997 | 1 | null | null | 3.0 | 2.70435 | 90.144997 | 90.144997 | null | null | null | 1 | 0 | 1 | 16 | 29 | 4.40794 | 100000 | 8 | 9 | 8 | 9 |

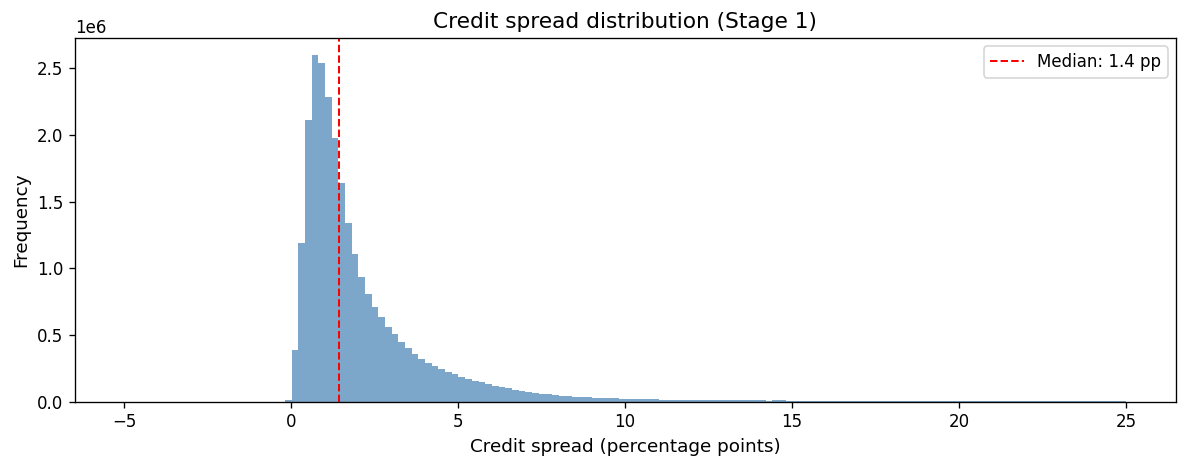

Credit spread distribution#

The credit spread is the yield premium a corporate bond pays over a duration-matched Treasury zero-coupon yield. It reflects credit risk, liquidity risk, and other bond-specific factors.

cs = (

s1.filter(

pl.col("credit_spread").is_not_null()

& (pl.col("credit_spread") > -0.05)

& (pl.col("credit_spread") < 0.25)

)

.select("credit_spread")

.collect()["credit_spread"]

.to_numpy()

)

fig, ax = plt.subplots(figsize=(10, 4))

ax.hist(cs * 100, bins=150, color="steelblue", alpha=0.7, edgecolor="none")

median_cs = np.median(cs) * 100

ax.axvline(

median_cs,

color="red",

linestyle="--",

linewidth=1.2,

label=f"Median: {median_cs:.1f} pp",

)

ax.set_xlabel("Credit spread (percentage points)")

ax.set_ylabel("Frequency")

ax.set_title("Credit spread distribution (Stage 1)")

ax.legend()

fig.tight_layout()

plt.show()

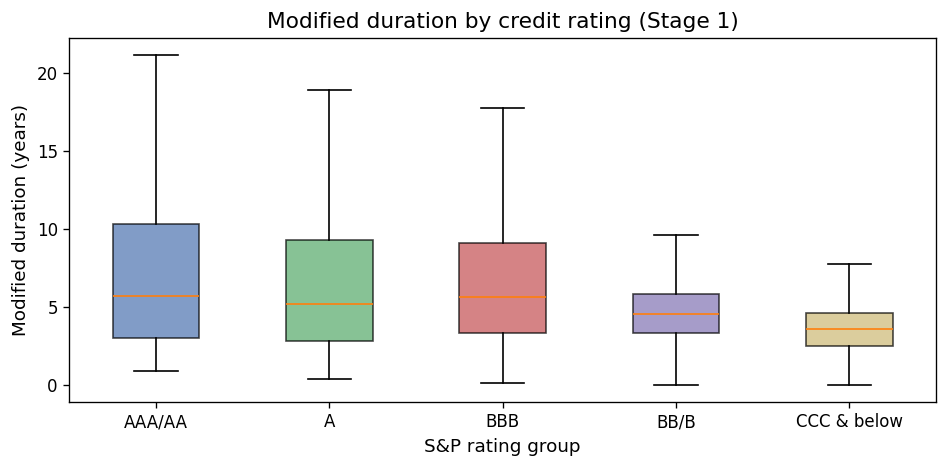

Modified duration by credit rating#

Investment-grade bonds (AAA through BBB) tend to have longer duration because they carry lower default risk and can issue at longer maturities. High-yield bonds (BB and below) tend to have shorter duration.

s1_dur = (

s1.filter(

pl.col("mod_dur").is_not_null()

& pl.col("sp_rating").is_not_null()

& (pl.col("mod_dur") > 0)

& (pl.col("mod_dur") < 30)

& (pl.col("sp_rating") > 0)

)

.select("mod_dur", "sp_rating")

.collect()

)

def _rating_bucket(r):

if r <= 3:

return "AAA/AA"

elif r <= 6:

return "A"

elif r <= 10:

return "BBB"

elif r <= 16:

return "BB/B"

else:

return "CCC & below"

s1_dur_pd = s1_dur.to_pandas()

s1_dur_pd["rating_group"] = s1_dur_pd["sp_rating"].apply(_rating_bucket)

order = ["AAA/AA", "A", "BBB", "BB/B", "CCC & below"]

data_by_group = [

s1_dur_pd.loc[s1_dur_pd["rating_group"] == g, "mod_dur"].values

for g in order

]

# Only keep groups with data

valid = [(g, d) for g, d in zip(order, data_by_group) if len(d) > 0]

order_valid = [g for g, _ in valid]

data_valid = [d for _, d in valid]

fig, ax = plt.subplots(figsize=(8, 4))

bp = ax.boxplot(data_valid, labels=order_valid, patch_artist=True, showfliers=False)

box_colors = ["#4c72b0", "#55a868", "#c44e52", "#8172b2", "#ccb974"]

for i, patch in enumerate(bp["boxes"]):

patch.set_facecolor(box_colors[i % len(box_colors)])

patch.set_alpha(0.7)

ax.set_xlabel("S&P rating group")

ax.set_ylabel("Modified duration (years)")

ax.set_title("Modified duration by credit rating (Stage 1)")

fig.tight_layout()

plt.show()

/var/folders/l3/tj6vb0ld2ys1h939jz0qrfrh0000gn/T/ipykernel_90126/3343011909.py:41: MatplotlibDeprecationWarning: The 'labels' parameter of boxplot() has been renamed 'tick_labels' since Matplotlib 3.9; support for the old name will be dropped in 3.11.

bp = ax.boxplot(data_valid, labels=order_valid, patch_artist=True, showfliers=False)

Bond age vs time-to-maturity#

s1_scatter = (

s1.filter(

pl.col("bond_maturity").is_not_null()

& pl.col("bond_age").is_not_null()

& pl.col("credit_spread").is_not_null()

& (pl.col("credit_spread") > -0.02)

& (pl.col("credit_spread") < 0.20)

& (pl.col("bond_maturity") > 0)

& (pl.col("bond_maturity") < 35)

)

.select("bond_age", "bond_maturity", "credit_spread")

.head(50_000)

.collect()

)

fig, ax = plt.subplots(figsize=(8, 5))

sc = ax.scatter(

s1_scatter["bond_age"].to_numpy(),

s1_scatter["bond_maturity"].to_numpy(),

c=s1_scatter["credit_spread"].to_numpy() * 100,

s=3,

alpha=0.3,

cmap="RdYlGn_r",

vmin=0,

vmax=8,

)

cbar = fig.colorbar(sc, ax=ax)

cbar.set_label("Credit spread (pp)")

ax.set_xlabel("Bond age (years since issuance)")

ax.set_ylabel("Time to maturity (years)")

ax.set_title("Bond age vs maturity, colored by credit spread")

fig.tight_layout()

plt.show()

7. Takeaways and Best Practices#

Always clean TRACE data before computing returns. Raw data contains cancellations, corrections, reversals, decimal-shift errors, and bounce-back errors. Using uncleaned data biases return estimates.

Use the FISD universe to restrict to standard US corporate bonds. Mixing in government, muni, ABS, or MBS trades will contaminate your sample.

Prefer volume-weighted prices (

prc_vw) over equal-weighted (prc_ew) when computing returns. EW prices over-weight small, noisy trades.Be aware of market microstructure noise. Even after cleaning, daily prices contain bid-ask bounce and dealer markup noise (Dickerson, Robotti, and Rossetti, 2024). Price-based signals (e.g., short-term reversal) may be spuriously profitable.

Avoid ex-post filtering. Do not condition your bond sample on future price availability or forward-looking criteria. Use only ex-ante filters with information available at portfolio formation (Dickerson, Robotti, and Rossetti, 2024, 2026).

Validate against known benchmarks. Compare your output to the Open Bond Asset Pricing (OBAP) database for duration, convexity, and credit spread validation.

References#

Dick-Nielsen, J. (2009). Liquidity biases in TRACE. Journal of Fixed Income, 19(2), 43–55.

Dick-Nielsen, J. (2014). How to clean enhanced TRACE data. Working paper.

Dickerson, A., Robotti, C., and Rossetti, G. (2024). Common pitfalls in the evaluation of corporate bond strategies. Available at SSRN: https://ssrn.com/abstract=4575879.

Dickerson, A., Robotti, C., and Rossetti, G. (2026). The Corporate Bond Factor Replication Crisis.