LSEG Datastream#

LSEG Datastream is a platform that provides access to a wide range of financial data, including futures data. Datastream is available via WRDS. WRDS does not provide real-time data access to Datastream, but it is still a valuable source of data for research. The Datastream data in WRDS is updated monthly. The data is the same as the data in LSEG Workspace (e.g., via Eikon).

Getting Started with Documentation#

Before searching for specific data, it’s recommended to familiarize yourself with Datastream’s documentation:

Visit the WRDS Datastream Documentation Page

Log in with your WRDS credentials

Review the available manuals and overviews to understand:

Data coverage and limitations

Search functionality

Available data types and formats

Mnemonic conventions

This documentation will help you navigate the platform more effectively and understand the data structure before proceeding with specific queries.

Finding Variables (in Datastream and in WRDS generally)#

WRDS provides a powerful variable search tool that allows you to search across all WRDS datasets, including Datastream. This can be particularly helpful when:

You’re unsure which dataset contains your variable of interest

You want to compare similar variables across different datasets

You need to find specific mnemonics or variable names

Using the WRDS Variable Search#

Navigate to the WRDS Variable Search Page

Log in with your WRDS credentials

Use the search functionality in several ways:

Search by keyword (e.g., “treasury futures”)

Filter by database (e.g., “Datastream”)

Browse by category

Use advanced search options for more specific queries

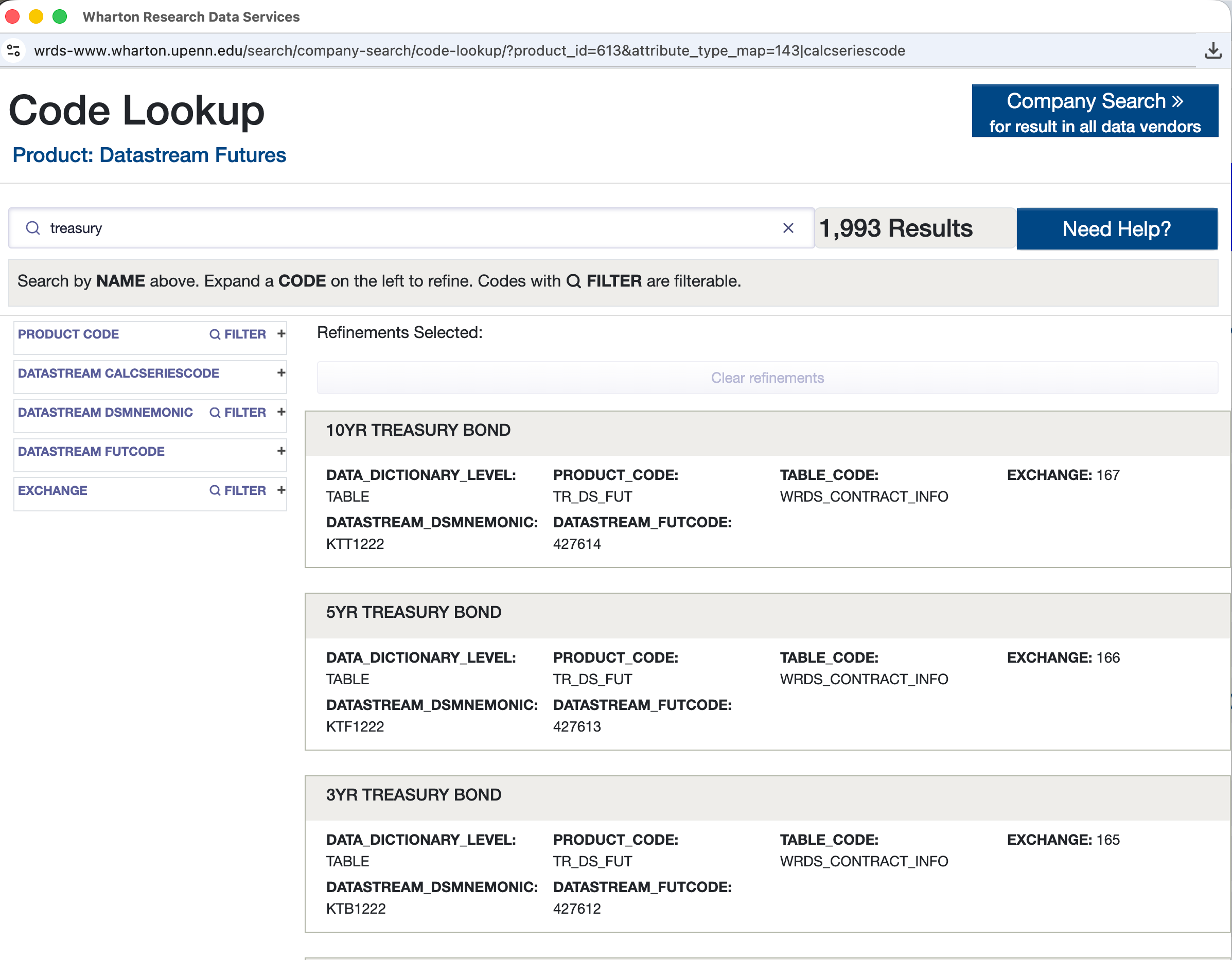

Using the Datastream Code Lookup Tool#

Navigate to the Datastream Future Contracts Query Form

Click on “Code Lookup: Datastream Futures”

Use the search functionality to find the code for the variable you are interested in

Search Tips#

Use quotation marks for exact phrase matches

Try different variations of terms (e.g., “Treasury”, “T-Note”, “Government Bond”)

Check variable definitions carefully as similar variables may exist across different datasets

Note the update frequency and coverage period for each variable

The variable search tool is particularly valuable when working with Datastream, as it can help you identify the correct mnemonics and understand what data is available before constructing your queries.

Treasury Futures Example 1#

Search https://wrds-www.wharton.upenn.edu/dynamic-query-form/tr_ds_fut/wrds_cseries_info/

Treasury Futures Example 2#

Let’s consider first an example of how to search for Treasury Futures data in Datastream via WRDS.

To effectively search for Treasury Futures data in Datastream via WRDS, follow these steps based on the available tools and mnemonic conventions:

1. Access Futures Data via WRDS Web Query#

WRDS provides a structured interface for retrieving futures data:

Navigate to the Thomson/Refinitiv section in WRDS and select Datastream.

2. Mnemonic Structure for Treasury Futures#

Datastream uses standardized codes for futures contracts:

Continuous series (front contract):

Format:[Symbol]CS00

Example:TYCS00for 10-Year Treasury Note futures (whereTYrepresents the underlying asset).CSindicates “continuous series” (auto-rolls to the next contract at expiration).00specifies the rollover timing (1st day of the new month).

Individual contracts (live or expired):

Format:LFUT[Symbol][L/D]

Example:LFUTTYLfor live 10-Year Treasury contracts orLFUTTYDfor dead (expired) ones.LFUT= List FuturesL= Live,D= Dead

3. Key Treasury Futures Symbols#

Common mnemonics for U.S. Treasury futures include:

Contract |

Base Symbol |

Example Continuous Series |

Example Individual Contracts |

|---|---|---|---|

2-Year Treasury Note |

|

|

|

5-Year Treasury Note |

|

|

|

10-Year Treasury Note |

|

|

|

30-Year Treasury Bond |

|

|

|

4. Search and Browse Tips#

Use WRDS Economic Indicators Filter: Narrow results by selecting “Futures” under asset classes and filtering by keywords like “Treasury” or “Bond”.

Consult Datastream Documentation: Access mnemonic lists and data dictionaries via WRDS’s Thomson/Refinitiv resources.

Verify Coverage: WRDS includes futures data but excludes fixed-income modules like bonds. For granular bond futures, consider cross-referencing with CRSP’s Treasury data.

5. Data Retrieval Example#

To download 10-Year Treasury Note futures:

Continuous series: Use

TYCS00for auto-rolling front-month data.Individual contracts: Use

LFUTTYLto retrieve all live contracts orLFUTTYDfor expired ones.Export Options: Output data in

.csv,.xlsx, or SAS formats via WRDS web queries.

Exploring the Futures Library via Python#

The WRDS web interface is useful for quick lookups, but programmatic access via Python is essential for reproducible research workflows. Connecting to WRDS from Python lets you run SQL queries against the Datastream library, iterate over products, and build datasets that feed directly into your analysis pipeline.

Example repository:

wrds_datastream/

— a set of 7 progressive scripts that teach you how to browse, search, and

retrieve futures data from the tr_ds_fut library.

Script |

What You Learn |

|---|---|

|

Survey tables, schemas, row counts, and sample rows |

|

List all available futures products with contract counts and date ranges |

|

Search by keyword (commodities, treasuries, equity indices) |

|

Inspect individual contracts: |

|

Fetch settlement prices (complete retrieval workflow) |

|

Compare term structures: commodity vs. Treasury futures |

|

Reference: pull 21 commodities + 4 Treasury futures |

The Datastream mnemonics described above (e.g., TYCS00 for the 10-Year

Treasury continuous series) are useful for identifying products in the WRDS web

interface, but when you query the underlying SQL tables you work with relational

keys instead — primarily contrcode (product type) and futcode (individual

contract).

Data Model: Library Structure and Key Relationships#

The tr_ds_fut library contains four key tables:

Table |

Description |

Scale |

|---|---|---|

|

Continuous series metadata (auto-rolling front contracts) |

Small catalog (~hundreds of rows) |

|

Individual contract metadata: |

~100k rows |

|

Daily prices by |

~30M+ rows |

|

Calculated series values (continuous contracts) |

~10M+ rows |

The tables are linked through a hierarchical relationship:

contrcode (product type, e.g. Gold = 2020, 10Y Treasury = 458)

└── wrds_contract_info (one row per contract, has futcode + delivery date)

└── wrds_fut_contract (daily prices per futcode)

Two-step retrieval pattern. Because metadata and prices live in separate tables, retrieving prices is always a two-step process:

Find contracts: Query

wrds_contract_infoto get thefutcodevalues for the product and date range you need.Fetch prices: Use those

futcodevalues to pull daily data fromwrds_fut_contract.

This separation keeps the price table lean (no repeated metadata) and lets you filter contracts by delivery date, last trade date, or other attributes before pulling potentially millions of price rows.

Highlights from the Example Scripts#

The sections below show key code patterns from the example repository. Each snippet is self-contained — you can adapt it directly for your own projects.

Searching for Products#

The search_products() function from 03_search_products.py queries

wrds_contract_info for products whose name matches a keyword:

def search_products(db, keyword):

"""Search for futures products by keyword (case-insensitive)."""

kw = keyword.lower().replace("'", "''")

query = f"""

SELECT contrcode, contrname,

COUNT(*) AS num_contracts,

MIN(startdate) AS earliest_start,

MAX(lasttrddate) AS latest_trade

FROM tr_ds_fut.wrds_contract_info

WHERE LOWER(contrname) LIKE '%%{kw}%%'

GROUP BY contrcode, contrname

ORDER BY num_contracts DESC

"""

return db.raw_sql(query)

A search for "treasury" returns results like:

Product Code Contracts From To

10 YEAR US TREASURY NOTE(CBT) 458 289 1982-03-31 2026-09-19

US TREASURY BOND(CBT) 268 343 1977-06-24 2026-09-19

5 YEAR US TREASURY NOTE(CBT) 510 198 1988-01-04 2026-09-19

2 YEAR US TREASURY NOTE(CBT) 599 146 1990-07-02 2026-06-30

...

The contrcode values in this output (458, 268, 510, 599) are the keys you use

in all subsequent queries.

Two-Step Price Retrieval#

From 05_pull_prices.py — the complete workflow for fetching settlement prices:

# Step 1: Find recent contracts for 10Y Treasury (contrcode=458)

query = f"""

SELECT futcode, contrcode, contrname, contrdate, startdate, lasttrddate

FROM tr_ds_fut.wrds_contract_info

WHERE contrcode = 458

AND lasttrddate >= '2024-01-01'

ORDER BY contrdate

"""

contracts = db.raw_sql(query)

# Step 2: Pull daily prices for those contracts

futcode_list = ",".join(str(int(f)) for f in contracts["futcode"].tolist())

query = f"""

SELECT futcode, date_, settlement, open_, high, low, volume

FROM tr_ds_fut.wrds_fut_contract

WHERE futcode IN ({futcode_list})

AND date_ >= '2024-01-01'

ORDER BY futcode, date_

"""

prices = db.raw_sql(query)

Step 1 returns the contract-level metadata (which delivery months exist, when

they last traded). Step 2 uses the resulting futcode values to pull the actual

daily price series.

Term Structure Snapshot#

From 06_term_structure.py — a single JOIN query that builds a cross-section of

all active delivery months on a given date:

query = f"""

SELECT ci.futcode, ci.contrdate, ci.lasttrddate,

fc.settlement, fc.volume

FROM tr_ds_fut.wrds_contract_info ci

JOIN tr_ds_fut.wrds_fut_contract fc

ON ci.futcode = fc.futcode

WHERE ci.contrcode = 458

AND fc.date_ = '2025-01-31'

AND fc.settlement IS NOT NULL

ORDER BY ci.contrdate

"""

term = db.raw_sql(query)

This returns one row per delivery month — the building block for analyzing term structure shape (contango vs. backwardation for commodities, or carry dynamics for Treasuries).

Tip

Script 07_pull_commodities_and_treasuries.py combines all of these patterns

into a single reference script that pulls 21 commodities and 4 Treasury futures.

Use it as a starting point for building your own research datasets.

Key Limitations#

WRDS updates Datastream data monthly, while LSEG Workspace offers real-time updates.

For intraday data or non-U.S. Treasury futures, use LSEG Workspace (access varies by institution).

By applying these conventions and tools, you can efficiently locate and extract Treasury Futures data in Datastream via WRDS.